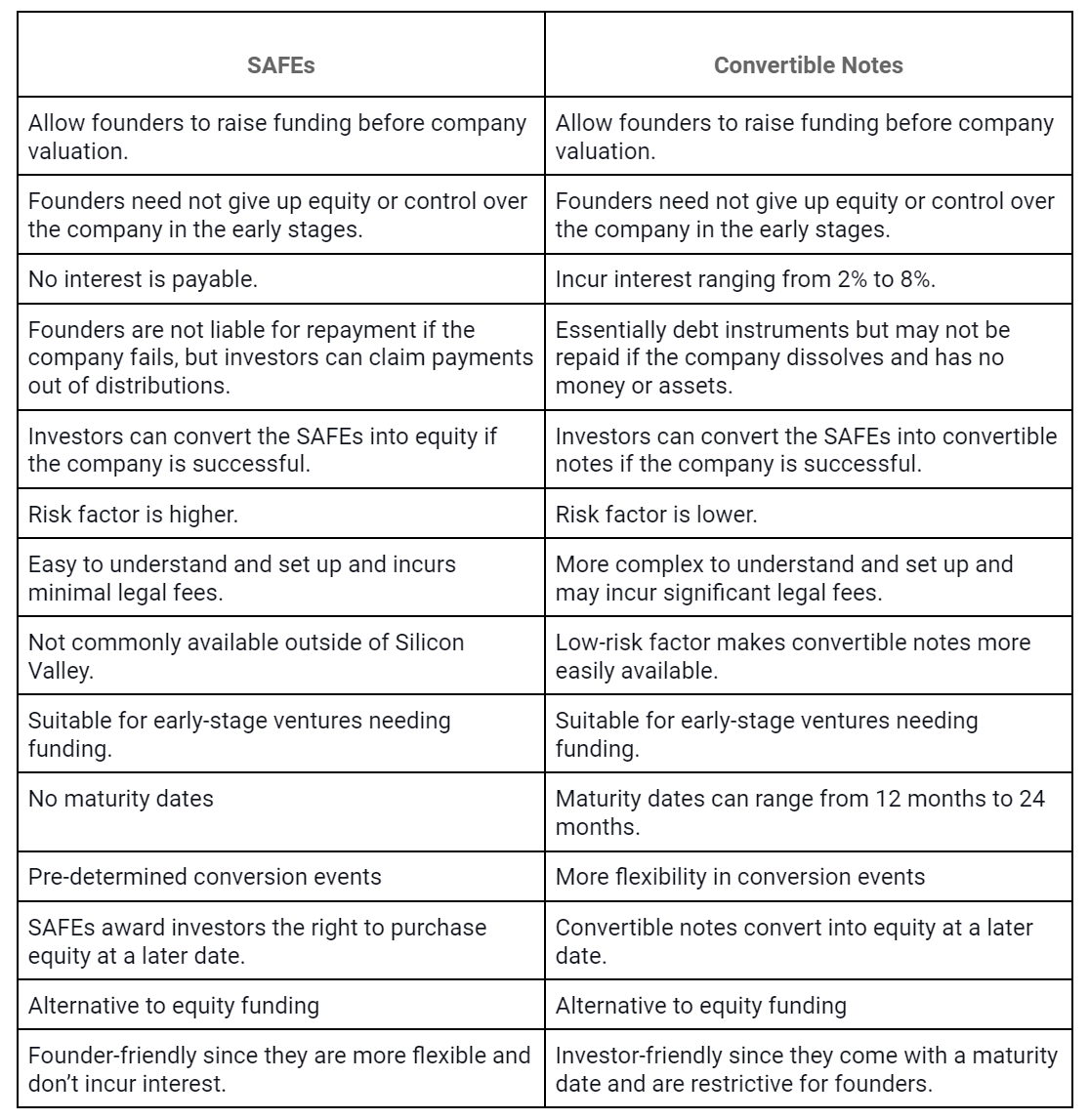

When looking for funding for your new venture, know the distinction between SAFEs vs. convertible notes. This skill can prove handy for startup founders who need more money after bootstrapping and using loans from friends and family members.

Reaching out to investors might not work well for you since they are hesitant to support new ventures. The success rates for startups are not exactly impressive, with at least 10% failing within their first year. Another 50% close doors by year five, and 90% will have folded by the time they reach year 10.

The risk factor is extremely high since the companies and their founders have yet to build a credible track record. Further, small companies may not have any assets to offer as collateral for the loans.

This information is not designed to discourage you. But to encourage you to scout around for other options. SAFEs and convertible notes are viable instruments to get you funding for the seed round. But without the need to value the startup or demonstrate that you have a robust customer base.

An added advantage is that you won’t have to give up equity or ownership stakes now. Nor do you need to cede control over the company’s decision-making. SAFEs vs. convertible notes won’t cost you substantial interest, so you can roll the company’s profits back into it to make it sustainable.

*FREE DOWNLOAD*

The Ultimate Guide To Pitch Decks

Understanding SAFEs

SAFE is the acronym for a Simple Agreement for Future Equity and is a form of convertible note. Startup founders can get money from investors to fund their company in exchange for these notes. SAFEs entitle investors to purchase equity in the company on the condition of a particular liquidity event.

Typically, this event occurs during the next funding round. The terms and conditions of getting capital via SAFEs may include a valuation cap or discount rate for investors. This provision allows them to offset some of the risk they take in backing a startup.

For instance, investors enter into a SAFE agreement with a new venture, offering capital worth $10M. Per the rights to purchase shares in the first priced funding round, the investor can get a 20% discount rate. Or, they can purchase shares at a valuation cap of $20M.

However, this discount is applicable only if the company is valued at or below the pre-determined cap. Let’s assume the startup launches a series A funding round with a valuation of $25M. Now that this is a priced round, the investor is entitled to convert the SAFEs.

However, the investor does not need to purchase at this valuation of $25M. But they can convert the SAFEs at a maximum valuation of $15M. If the company is valued at $15M, investors can buy in at a 20% discount of $12M only.

The Y Combinator, a Silicon Valley incubator, developed the concept of SAFEs in 2013. There are a few distinctions between SAFEs vs. convertible notes.

Raise Capital Smarter, Not Harder

- AI Investor Matching: Get instantly connected with the right investors

- Pitch & Financial Model Tools: Sharpen your story with battle-tested frameworks

- Proven Results: Founders are closing 3× faster using StartupFundraising.com

Repayment Terms and Conditions for SAFEs

SAFEs don’t come with maturity dates, and investors cannot convert their agreements before the next funding round. The time interval can be six months or six years. Further, if the startup fails before the conversion, founders are not liable for repayment since they are not debt instruments.

However, investors get priority above the company’s founders for repayments. In the case of distributions, after the startup fails, SAFE investors receive a part of the available liquidity. Repayments are in proportion to their ownership in the company.

Keep in mind that in fundraising, storytelling is everything. In this regard, for a winning pitch deck to help you here, take a look at the template created by Silicon Valley legend Peter Thiel (see it here) that I recently covered. Thiel was the first angel investor in Facebook with a $500K check that turned into more than $1 billion in cash.

Remember to unlock the pitch deck template that is being used by founders around the world to raise millions below.

Understanding Convertible Notes

Convertible notes work similarly to business loans except that the founder doesn’t need to repay the debt. Instead, the note automatically converts into equity or preferred stock at a pre-determined trigger that can be a milestone. Or any other event in the startup.

For instance, the company reaches a valuation of $30M and raises $5M in funding. Or if the startup goes through an Initial Public Offering (IPO) or enters into an M&A transaction for sale. Conversion can also take place if investors and founders enter into an agreement.

Typically, convertible notes include a valuation cap, discount rate, and maturity date in their terms and conditions. Accordingly, the loan will convert even if the pre-determined trigger does not take place. This date is usually set for between 12 months and 24 months from the loan date.

Convertible notes combine features of equity financing and debt and incur interest similar to any other loan. However, founders can raise money without valuing the company. Although convertible notes convert into equity, you have the option to repay the loan to avoid dilution.

For instance, you accept an investment of $100,000 at an 8% interest rate. You’ll pay $108,000 at the end of the maturity date if you’ve been unable to raise a priced round. Though interest is payable on convertible notes, the payments need not be in the form of cash only. Investors receive a higher number of shares to compensate for interest.

SAFEs vs. Convertible Notes – The Suitable Option

Understand How the Valuation Cap Works in SAFEs vs. Convertible Notes

Investors purchasing convertible notes or SAFEs in a startup get compensation for taking on the risk with valuation caps. The cap is the upper limit on the company’s valuations when the instruments convert into equity.

Or the maximum valuation used to calculate the stock price at which the investors’ money converts into stock. For instance, the company is valued at $7M or higher, but the valuation cap is $1M. By investing $100,000 in the company, investors can get a 10% equity stake in the startup.

Caps are also crucial for founders because they limit the amount of equity or ownership you must give up. Say the company values at significantly higher pricing than your grade limit at the next funding round. In that case, you may have to issue far more shares than you want to give up.

Caps allow you to place limits so you can determine the appropriate amount of equity you can cede.

Termination Conditions

SAFEs vs. convertible notes, both instruments come with terms and conditions that determine how payments will be made in case of certain events before conversion. For instance, the company may enter into an M&A transaction, and control may be transferred to the buyer. Or, you may take it to an IPO.

SAFEs typically include provisions to handle these events, which allow investors to convert into equity per the valuation limit. This conversion is possible since SAFEs don’t have a maturity date. However, if the startups goes bankrupt, SAFEs don’t require repayment since they are not loans.

Similarly, since convertible notes are a form a debt, and don’t need to be repaid if the company goes bankrupt. However, since these notes have a due date of 12 months to 24 months, the next funding round must take place before this time.

If the startup has been unable to raise capital before the due date, it must repay the loan’s principal and interest. Alternatively, you can convert the debt into equity or negotiate with the loanmakers for an extension on the payment date.

What do investors look for in a business? How to come up with an investor worthy business idea? Check out this video where I have explained in detail how its done.

From the Investors’ Perspective

SAFEs vs. convertible notes–investors are more interested in convertible notes since they offer more benefits. Not only do they come with a maturity date and interest rates, but they also have binding terms. Investors can negotiate for renewals and collateral like company assets or IP.

On the flip side, SAFEs are readily available and require a minimum of legal expertise. The structure is fairly standard, which helps investors complete the funding process quickly. Convertible notes typically involve different variables, and negotiating their terms and conditions is a lengthy process.

Founders and investors need to get legal direction and advice before signing the Note Purchasing Agreement (NPA). Or the agreement that outlines the terms and conditions for the convertible notes.

From the investors’ perspective, SAFEs lack a maturity rate and interest rate that can extend their timeline. Investors cannot predict accurately when their SAFEs will convert into equity. Further, since SAFEs only have a valuation cap but no discounted pricing, they may not seem like a viable deal.

As a rule, tech startups prefer to go with SAFes, possibly because founders get the funding they need quickly. They can get their companies up and running in no time. However, finding investors willing to make SAFEs can present a challenge.

The higher risk factor in SAFEs that does not entitle investors to compensation is also a deterrent. At best, they can request a portion of the distributions after the startup and its assets are sold. For this reason, investors may require higher returns to offset the risk.

Founders may also be hesitant to use SAFEs since they translate into losing ownership and control.

A409a Rating for SAFEs

Although founders can avoid valuing the company to pitch for funding, investors may require that they get the A409a rating. This rating evaluates the viability of the startup as an investment option by taking into account other factors.

The A409a rating can be executed at different stages of the startup, including the pre-revenue stage. Investors may consider factors like the total number of employees, the total revenue earned, and the company’s capital structure.

This rating can form the basis of the funding amount investors are willing to offer the startups. It can also influence the terms and conditions for repayment. The A409a rating is typically conducted by their parties to appraise the startup’s Fair Market Value (FMV).

In Conclusion

SAFEs vs. convertible notes: choosing the appropriate option depends on where your business is at. Going with convertible notes allows you to delay valuation and dive into starting the company. But, going with SAFEs may require you to get an A409a rating.

Regardless of the option you go with, be aware that, ultimately, both instruments convert into equity. And, unless you pay off the loan, you’ll expect dilution and ceding ownership and control. Investors may also require board seats, which can mean giving up decision-making powers.

Although SAFEs have more advantages, attracting investors could be more challenging. In that case, founders have no option left but to offer convertible notes.

Take your time assessing the pros and cons of both instruments before you make the optimum choice.

You may find our free library of business templates interesting as well. There you will find every single template you will need when building and scaling your business completely for free. See it here.

Facebook Comments